Leasing on a Deadline: What Student Housing Demands Right Now

The student housing sector enters the spring 2026 leasing push in a deceptively comfortable position. Occupancy for the 2025-2026 academic year hit 95.1%, one of the strongest results in recent memory. Capital is flowing back in. Institutional investors are competing for portfolios near flagship universities.

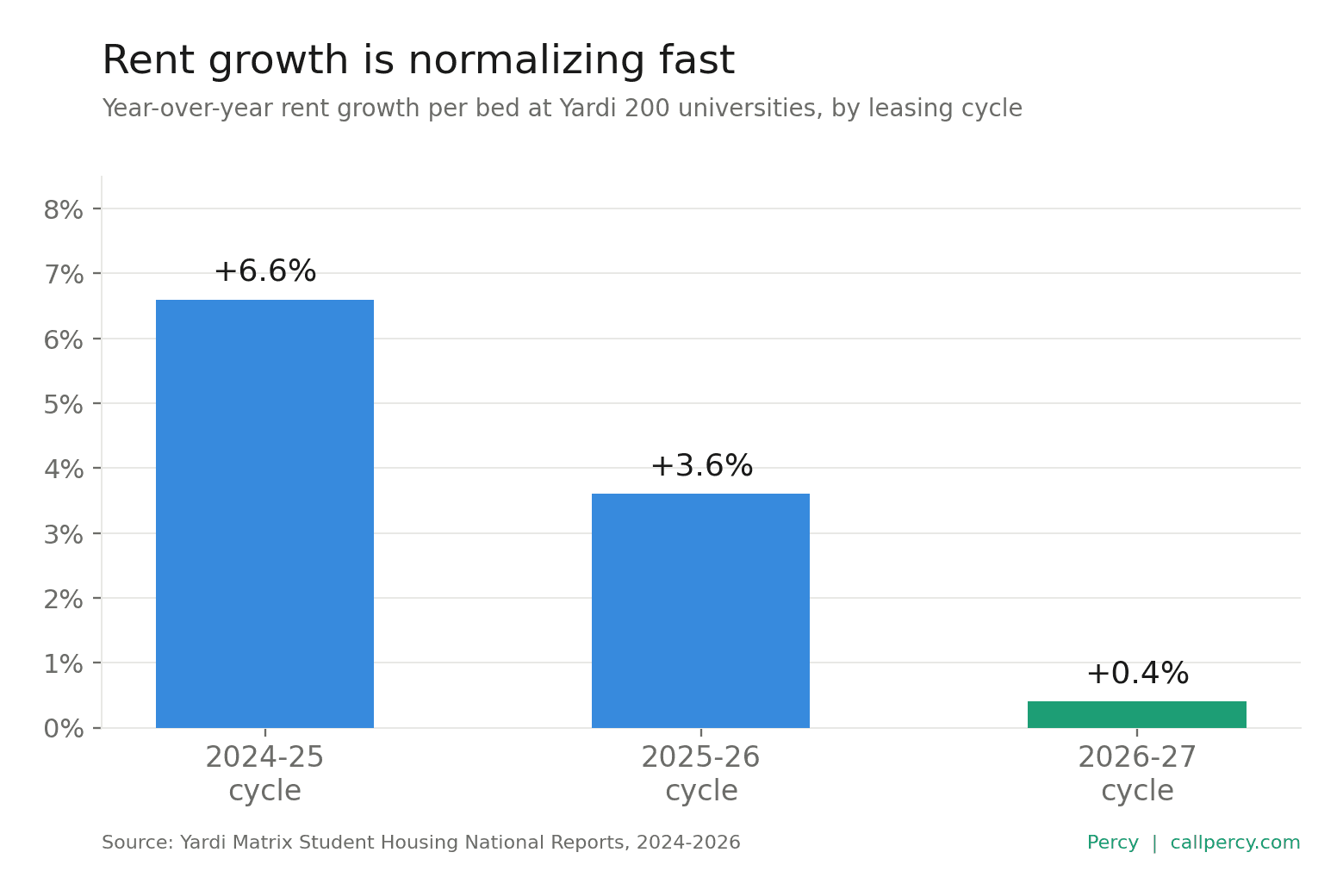

But the leasing environment underneath those numbers has shifted, and the shift has a direct implication for how operators staff their on-site teams. After two years of post-pandemic rent surges (6.6% growth two years ago, 3.6% last year), the cycle is normalizing. Preleasing for the 2026-2027 cycle reached an estimated 58.6% in February, according to the Yardi Matrix March 2026 Student Housing National Report. Average rent per bed reached $925, up just 0.4% year over year. Roughly 28,000 to 30,000 new beds are expected to deliver for Fall 2026 across 37 campuses.

The bottom line for operators: the market that rewarded average leasing teams with strong results is giving way to one where the quality of your leasing talent shows up directly in your preleasing pace, your concession spend, and your revenue per bed. The communities pulling ahead are not doing it with better floor plans. They are doing it with better people.

A Market of Haves and Have-Nots

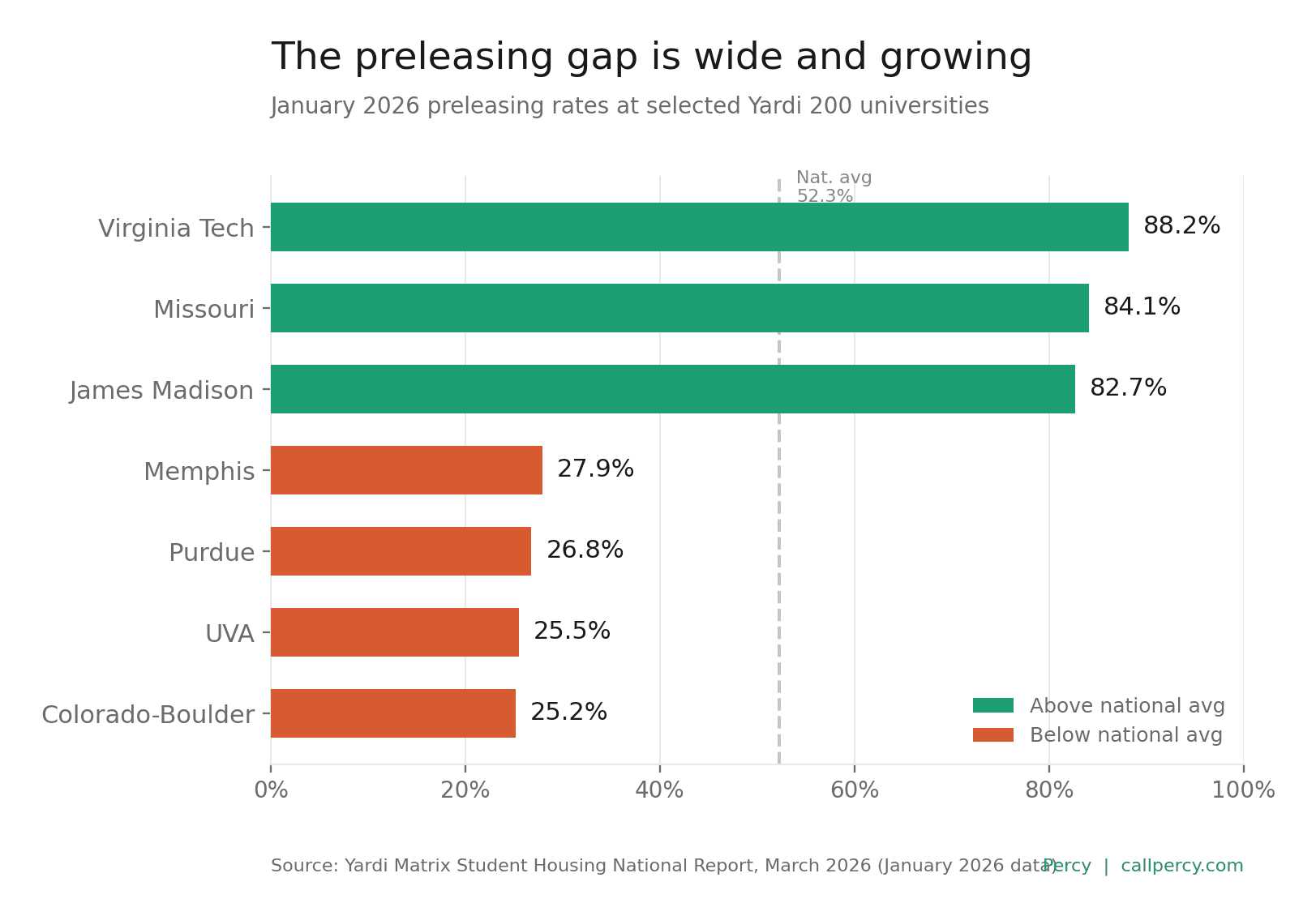

The national preleasing figure masks a sharp split. As of January, Virginia Tech led surveyed markets at 88.2% preleased. The University of Missouri sat at 84.1%. James Madison at 82.7%. These communities made staffing, pricing, and marketing decisions months ago, and the results are showing.

On the other end, 39 schools were under 30% preleased. Many sit in markets with active construction pipelines: Memphis at 27.9% with 705 beds underway, the University of Virginia at 25.5% with over 2,300 beds in the pipeline, Colorado-Boulder at 25.2% with more than 1,200 beds coming. Markets like Purdue and the University of Tennessee, where recent and incoming supply has stacked up, are seeing some of the sharpest rent pressure, with select submarkets pulling back 8 to 10% year over year.

Nearly half of all Yardi 200 markets posted year-over-year rent declines in January, averaging negative 4.6%. Concessions averaged 8.5% of asking rent in 2024 (the highest since 2015), with more than a third of beds now carrying some form of incentive. Even as February's national average ticked up to $925, the gap between the top and bottom of the board keeps widening.

When operators look at that gap, the instinct is to focus on product, location, or pricing strategy. All of those matter. But across markets with comparable supply dynamics, the variable that explains the difference most often is the team on site.

What This Means for Hiring

Two years ago, when rents were climbing 6-7% annually and nearly every market was pushing toward full occupancy, student housing leasing looked a lot like order-taking. Demand outpaced supply. Prospects showed up ready to sign. Operators could staff for friendliness and follow-through and the market did the rest.

That version of the job is fading. Today, leasing professionals in student housing are working in an environment where the cycle starts earlier (many properties now target 50% preleased before the spring semester begins), pricing power is flatter, and the competition down the street may be offering a better deal on a newer product. The prospect who toured last week has three other options, and the parent writing the check is comparing value more carefully than they were in 2022.

The skill set this demands is different, and operators who are hiring or evaluating their teams should be screening for it explicitly. The leasing professionals producing results in this cycle tend to be strong at objection handling, particularly around price. They use CRM and revenue management tools to spot prospect hesitation early rather than waiting for a lost lease to surface in the data. They hold parent-facing value conversations that go beyond amenity lists, which is why cross-training with community managers is becoming a competitive advantage at the properties doing it well. And they treat the immovable August move-in deadline not as a source of panic but as a forcing function for revenue protection: every week of delay in closing a prospect is margin left on the table.

If you are hiring for a student housing leasing role right now, the interview question is no longer "tell me about your leasing experience." It is "tell me about a cycle where preleasing was behind pace and what you did about it."

The Demographic Backdrop

A longer-term reality makes all of this more urgent. According to the WICHE "Knocking at the College Door" projections, the number of U.S. high school graduates peaked in 2025 and is expected to decline steadily from here, potentially by as much as 13% by 2041. Florida, Texas, Tennessee, and much of the Southeast are projected to keep growing. Large portions of the Midwest and Northeast will see shrinking graduating classes for years to come.

For operators near large flagship publics in growth states, this is manageable. For operators at smaller schools or in regions facing demographic headwinds, the leasing team becomes the difference between a stable asset and a struggling one. When the prospect pool tightens, the ability to convert a higher percentage of tours, retain more renewals, and defend rate against concession pressure is not a nice-to-have. It is the revenue strategy. And that strategy is only as strong as the people executing it.

The Season Is Already Underway

Student housing does not wait. The 2026-2027 leasing cycle is deep into its critical window, and that window is narrowing fast. Properties that are 80%+ preleased made their staffing and strategy decisions months ago. Properties sitting below 30% are playing catch-up against a deadline that does not move.

The market is healthy overall. But "overall" does not lease a single bed. The results are local, property-specific, and determined by the people on site executing in a compressed timeframe that offers very little room to recover from a slow start. For operators still evaluating their leasing bench, the time to act is not before the next cycle. It is now, while this one is still in play.

—

Percy Multifamily Recruiting specializes in student housing leasing consultants, leasing managers, community managers, and maintenance roles. We help operators build teams that thrive in competitive, deadline-driven cycles across conventional, affordable, and student housing. If you're strengthening your leasing team for Fall 2026, contact us to discuss how we can deliver talent that turns market normalization into on-site wins.